A · Current production page (faithful recreation). Status said twice, eight equal stats, four dashes wearing the same suit as facts, flat prose everywhere.

- Occupancy leader of the comp set: MPI 121.8, RGI 110.7 (Apr 2026 STAR R12)

- Margin gap is the HOURP shape: 17.3% GOP T-12 vs THM 30%+ norm

- YTD Apr 2026 ramping: revenue $4.99M, EBITDA $358,580 (7.19%) vs -$333,409 prior year

- PIP-sized hole in the cap stack: approved PIP-011515 ~115 items, $13-19.7M writeup estimate ($41.5-63K/key); entry ticket to the flag, valid only to 17-Feb-2027

- AHJ enforcement in flight: fire pump YELLOW-TAGGED ($29,140 replacement 50% deposited), cracked boiler $51,582, RTU B chiller $188,870

- Revenue quality: T-12 flattered by Jan-Apr 2026 contract/group surge while ADR fell -7.4% YoY

- Pricing guidance + receivership process (court caption, approval timeline, stalking-horse rights) - ask Joe Cuomo

- Hilton PIP economics: key money, FRCM-only feasibility, D/D deferral - swings financeable price ~$7M+

B · Ive's five changes, nothing added. One stage voice. The stat strip leads with what matters. The thesis sentence lands in bold at a readable measure. Every bullet gets a bold lead phrase. Unknowns retire to one quiet line.

- Occupancy leader: MPI 121.8, RGI 110.7 (Apr 2026 STAR R12)

- The HOURP margin shape: 17.3% GOP T-12 vs THM 30%+ norm

- Ramping into the sale: YTD Apr EBITDA $358,580 vs -$333,409 prior year

- PIP-sized hole in the cap stack: ~115 items, $13-19.7M estimate, valid only to 17-Feb-2027

- AHJ enforcement in flight: fire pump yellow-tagged $29,140, boiler $51,582, chiller $188,870

- Revenue quality: Jan-Apr contract surge flatters T-12 while ADR fell 7.4% YoY

- Pricing guidance + receivership process: court caption, timeline, stalking-horse rights. Ask Joe Cuomo.

- Hilton PIP economics: key money, FRCM-only feasibility. Swings financeable price ~$7M+.

C · Walk-sheet DNA. The tour page's dark hold-in-your-head hero comes to the desktop: four numbers, the one question that matters, then Ive's typography below. Boldest change, same data.

DoubleTree by Hilton Houston Intercontinental Airport

- Occupancy leader: MPI 121.8, RGI 110.7 (Apr 2026 STAR R12)

- The HOURP margin shape: 17.3% GOP vs THM 30%+ norm

- PIP-sized hole: $13-19.7M entry ticket, clock runs to 17-Feb-2027

- AHJ enforcement: yellow-tagged fire pump, boiler, chiller in flight

- Pricing + receivership process: ask Joe Cuomo

- Hilton PIP economics: swings the financeable price ~$7M+

D · Stitch-generated layout study (Google Stitch, Gemini lane, project 17622345829196036649). Generated from the same brief: lender-grade hierarchy, four-stat strip, bolded thesis close, pursue/kill split. NOTE: the open-question texts in this image (Union status, Tax abatement, Liquor license) are Stitch's invented placeholders, not real H156 data; judge the layout, not those words.

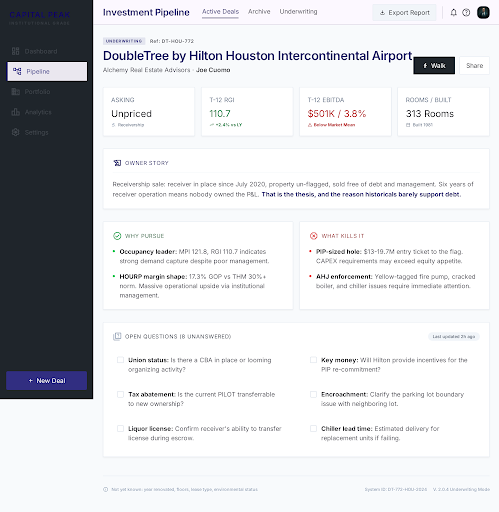

E · Ive's structure, Stitch's directness. Real data throughout. From D: the ref breadcrumb, captioned stat cards, colored section headers, two-column questions with an updated stamp. From B: the bolded thesis, lead-phrase bullets, one stage voice, the quiet unknowns line.

- Occupancy leader: MPI 121.8, RGI 110.7 (Apr 2026 STAR R12)

- The HOURP margin shape: 17.3% GOP T-12 vs THM 30%+ norm

- Ramping into the sale: YTD Apr EBITDA $358,580 vs -$333,409 prior year

- PIP-sized hole: $13-19.7M entry ticket to the flag, valid to 17-Feb-2027

- AHJ enforcement in flight: yellow-tagged fire pump $29,140, boiler $51,582, chiller $188,870

- Revenue quality: Jan-Apr contract surge flatters T-12, ADR fell 7.4% YoY

- Pricing + receivership process: ask Joe Cuomo

- Room mix (D/D count): biggest single PIP swing

- 2024 Other Non-Op $984K: line-item breakdown

- Contract/crew accounts: rates, terms, expirations

- Hilton PIP economics: swings price ~$7M+

- OM/CIM access: CA at properties.alchemyrea.com

- Full CapEx backlog: roof, elevators, risers

- HCAD facts: floors, SF, 2026 protest status